SB 322: Delaware Should Not Put School Property Taxes on Autopilot

Updated: 6 days ago

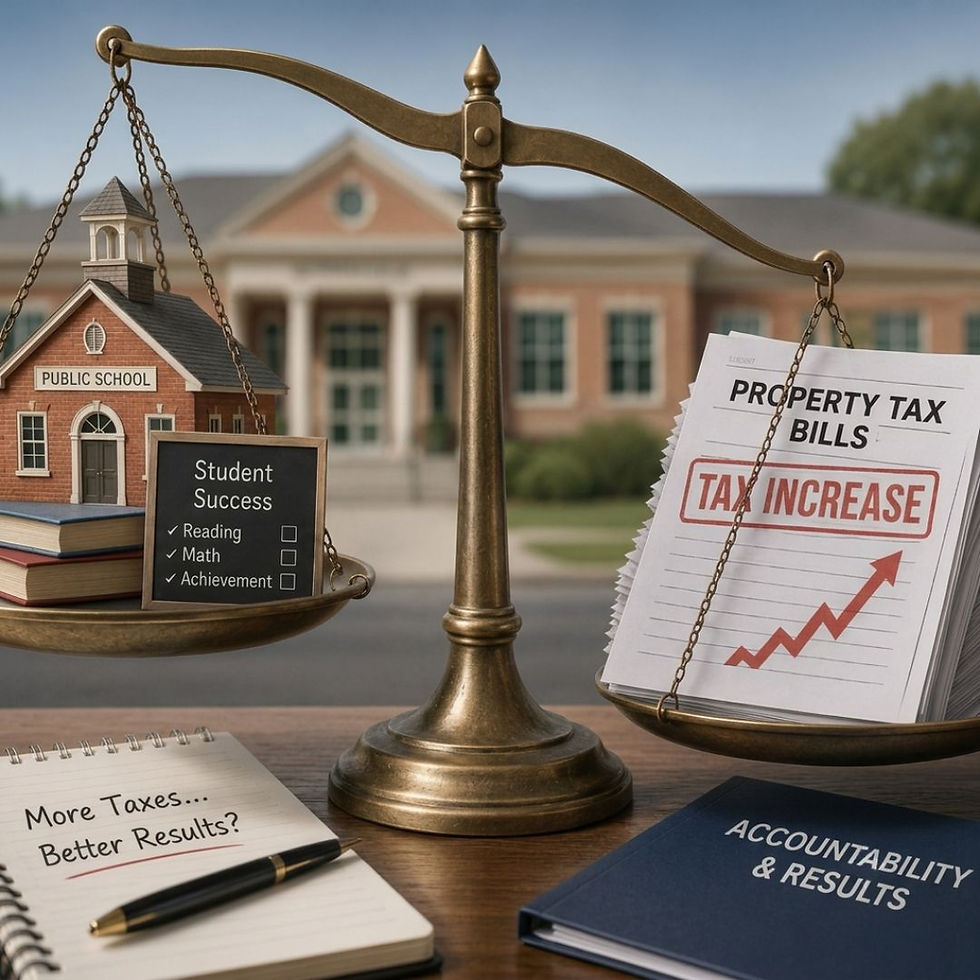

Delaware’s school-finance system has real problems, but automatic annual tax increases are NOT the solution. SB 322 moves Delaware toward a system in which school districts impose recurring annual property-tax increases without voters’ approval while educational outcomes remain among the weakest in the nation.

How SB 322 Expands School Taxing Authority

SB 322 does two important things. First, it replaces a 10% post-reassessment tax increase cap with a formula tied to the district's prior-year operating revenues and the average growth rate of taxable property since the previous reassessment.

Second, and more troubling, SB 322 would allow school districts to raise school property taxes by up to 2% annually without a referendum, provided the district’s “operational reserve balance” does not exceed 10% of annual revenue.

A 2% annual increase may sound modest, but compounded over 10 years, it amounts to a 21.9% increase. Using the New Castle County tax rate formula, for a $378,000 home in the Christina School District paying $3,023 in school property taxes, a recurring 2% annual increase would become approximately $3,685 after 10 years - costing the homeowner about $662 - before considering any other tax increases, reassessments, or general household inflation.

Minimal Statewide Enrollment Growth Weakens the Case for SB 322

Delaware’s annual student count (also called the unit count) includes public school students enrolled and in attendance during the last 10 school days of September and is the basis for Delaware school funding. According to the Delaware Department of Education, from 2015 to 2025, total annual enrollment in Delaware district schools grew by only 0.38%, an average increase of only 34 students per year statewide. Given such minimal statewide enrollment growth, the case for a new statewide mechanism allowing recurring tax increases deserves careful scrutiny. At the same time, that statewide figure masks significant differences among districts, with some growing rapidly while others are shrinking.

It is true that some districts face enrollment pressure. Cape Henlopen and Appoquinimink, for example, have 10-year growth rates of 30.2% and 24.9%, respectively. However, other districts have declined sharply. Christina, Colonial, and Red Clay have lost 17.7%, 15.3%, and 10.9% of their enrollment, respectively. Why do these districts need the authority for an automatic, annual tax increase of 2%, without taking the issue to a vote by referendum?

It is clear from this data that any case for higher taxes should be district-specific, tied to actual enrollment, student need, inflation, and demonstrated efficiency.

Why SB 322 May Encourage Districts to Spend More

SB 322 says districts cannot use the 2% authority if their “operational reserve balance” exceeds 10% of annual revenue. But that term is NOT defined in code. Does “annual revenue” mean total district revenue, local revenue, current-expense revenue, discretionary revenue, or all-funds revenue? Does “operational reserve” mean audited fund balance, projected cash balance, unencumbered local balance, or another Department of Education measure?

More importantly, penalizing reserve holdings incentivizes districts to reduce them to maintain their free taxing authority. In essence, SB 322 creates an incentive for districts to reduce reserves so they can increase spending. Instead, Delaware should create incentives to allocate existing spending more efficiently.

Delaware’s Educational Results Are Terrible

According to Delaware’s Fiscal Year 2026 budget, approximately one-third of Delaware’s spending goes to K-12 education (District and Charter Operations), yet Delaware’s educational results are among the worst in the nation. According to The Nation’s Report Card, 40% of Delaware eighth graders and 45% of Delaware fourth graders scored below Basic in reading on the 2024 National Assessment of Educational Progress (NAEP). Similarly, a 2024 Urban Institute analysis of demographically adjusted student performance ranked Delaware 48th in the nation in eighth-grade math and reading.

If lawmakers believe referenda are too blunt or disruptive, they should replace them with a stronger compact between districts and taxpayers. Funding growth should be tied to publicly available, measurable outcomes such as those shown in the table below.

Accountability measure | What districts should report by school before using automatic taxing authority |

Third grade reading improvement | Current proficiency, three-year trend, and targeted improvement |

Eighth grade math improvement | Current proficiency, 5-year NAEP/state assessment trend, and intervention plan |

Chronic absenteeism reduction | District rate, subgroup rates, and reduction target |

Discipline/safety metrics | Incidents, suspensions, school-climate data, and corrective strategy |

Postsecondary readiness | Graduation quality, career pathways, college readiness, and remediation indicators |

Special-education service outcomes | Identification trends, service delivery, compliance, and student progress |

Administrative cost containment | Central-office spending, staffing ratios, and overhead as share of budget |

Furthermore, Delaware should require publicly available efficiency audits conducted by the independently elected State Auditor before districts exercise automatic taxing authority. Those audits should review central-office staffing, procurement, transportation, facilities, energy costs, vendor contracts, administrative overhead, and program duplication.

Taxpayers Deserve Accountability Before Automatic Tax Increases

As written, SB 322 removes voter oversight while rewarding fiscal mismanagement and providing additional taxing authority regardless of educational underperformance.

Property taxes are paid from household cash flow, not from assessed value. Seniors on fixed incomes, young families buying homes at today’s interest rates, working-class homeowners, small landlords, and small businesses all face rising costs from insurance, utilities, maintenance, food, health care, and borrowing. An automatic school-tax escalator may be administratively convenient, but it is indifferent to a taxpayer’s ability to pay, the needs of a specific district, or educational outcomes.

Tax increases should be earned through results and approved by voters—not granted automatically by statute.

Comments